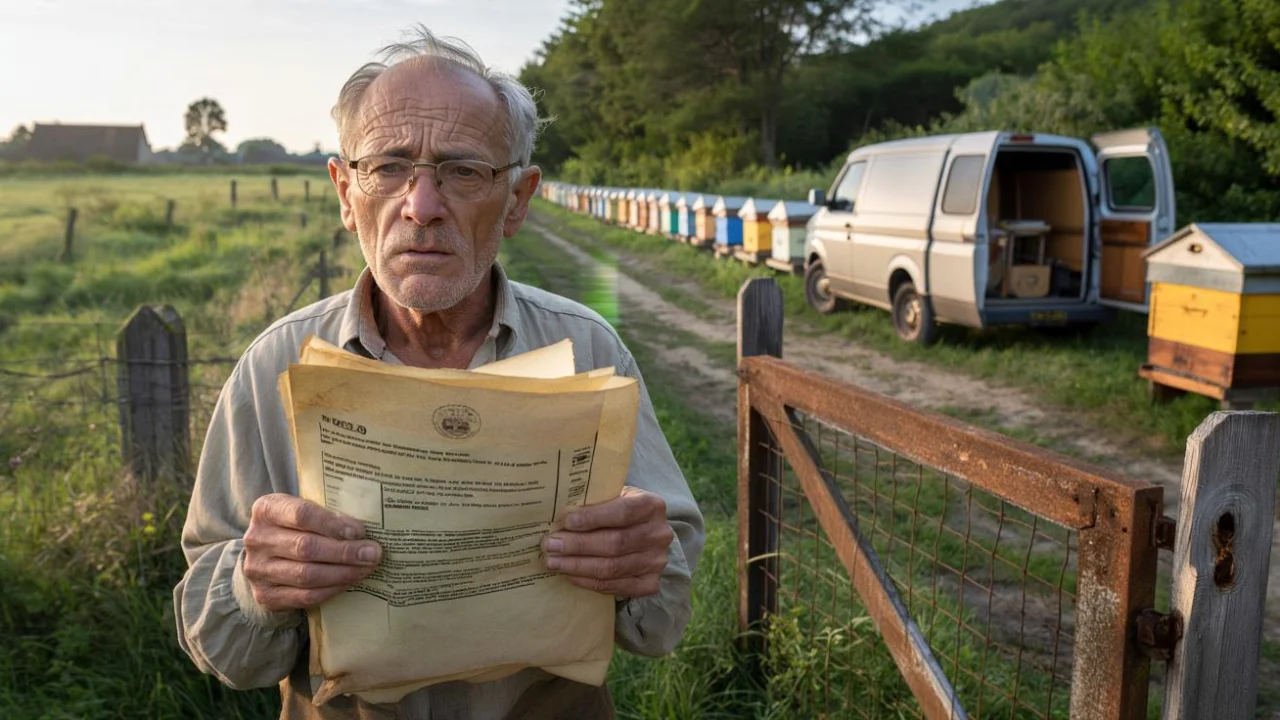

Margaret stared at the official envelope on her kitchen table, her morning coffee growing cold. At 68, she’d learned to recognize trouble by its government letterhead. Inside was an agricultural tax bill for $3,200 – nearly half her monthly Social Security check. All because she’d let her neighbor’s son keep a few beehives on her unused back acre three summers ago.

The worst part? She’d done it to help. Tommy was just starting his honey business, couldn’t afford land rent, and her property was sitting there doing nothing anyway. A simple handshake deal between neighbors. No paperwork, no fuss, just good people helping good people.

Now she was facing a tax burden that could force her to sell the land her father left her. The bitter lesson? Sometimes kindness comes with a price tag nobody mentions upfront.

When Good Deeds Trigger Unexpected Tax Consequences

Margaret’s situation isn’t unique. Across rural America, property owners are discovering that allowing agricultural activities on their land – even small-scale operations like beekeeping – can dramatically change their tax status. The agricultural tax bill often arrives months or years after the arrangement begins, catching landowners completely off guard.

Tax assessor Sarah Chen from rural Ohio explains: “Once land is used for commercial agriculture, even if the owner isn’t the farmer, the property classification changes. Many people don’t realize they’re suddenly liable for agricultural taxes, special assessments, and sometimes back taxes.”

The problem stems from how tax authorities define “agricultural use.” It doesn’t matter who owns the land or who profits from the farming activity. If commercial agriculture happens on your property, you become responsible for agricultural taxes associated with that use.

Property tax attorney Michael Rodriguez sees these cases regularly: “Landowners think they’re just being neighborly, but they’re unknowingly entering into what tax authorities consider a commercial agricultural arrangement. The tax implications can be severe.”

The Hidden Costs of Informal Land Arrangements

The financial impact of these surprise agricultural tax bills varies significantly by state and property size, but the consequences are consistently harsh for unprepared landowners. Here’s what property owners need to know:

| Tax Consequence | Typical Cost | When Applied |

|---|---|---|

| Agricultural use assessment | $2-15 per acre annually | Immediately after classification change |

| Special district fees | $50-500 per year | If property is in agricultural district |

| Back taxes and penalties | 3-7 years of accumulated charges | When reclassification is discovered |

| Loss of homestead exemption | $200-2000 annually | If residential exemptions are affected |

The most devastating aspect is often the retroactive nature of these bills. Tax authorities can demand payment for previous years once they discover the agricultural activity, even if the landowner was completely unaware of their obligations.

Key warning signs that your property might trigger agricultural taxation:

- Any commercial farming activity, regardless of scale

- Livestock grazing arrangements, even temporary

- Beehives operated by commercial beekeepers

- Crop sharing agreements

- Equipment storage for agricultural operations

- Hay cutting or timber harvesting by third parties

The Brutal Reality of Modern Neighborly Help

What makes these stories particularly painful is how they expose the harsh intersection between traditional community values and modern bureaucratic systems. The informal handshake deals that once defined rural life now carry hidden legal and financial risks.

Rural sociologist Dr. Amanda Foster has studied this phenomenon: “We’re seeing the breakdown of informal community support systems because people are afraid of unintended consequences. The tax system penalizes the very neighborliness that rural communities depend on.”

Margaret’s story took another painful turn when she approached Tommy about sharing the tax burden. The young beekeeper, struggling with his own business expenses, couldn’t help with the agricultural tax bill. Their friendly arrangement soured into resentment and legal threats.

“I felt stupid and used,” Margaret admits. “Here I was trying to help a kid get started, and it ended up costing me thousands while he got tax breaks as the ‘farmer.’ The system rewards the person making money and punishes the person being generous.”

This dynamic reveals a fundamental unfairness in how agricultural taxation works. The actual farmers often qualify for exemptions and subsidies, while property owners who enable their operations face the full tax burden without any of the profits.

Property owners who find themselves facing unexpected agricultural tax bills have limited options. They can challenge the reclassification, but success requires proving the land isn’t actually used for commercial agriculture – difficult when beehives or equipment are clearly visible.

Some attempt to formalize arrangements after the fact, creating written leases that shift tax responsibility to the agricultural user. However, many small-scale farmers can’t afford additional tax burdens, leaving property owners trapped.

Protecting Yourself from Tax Surprises

The harsh lesson from these cases is clear: no land arrangement is too small or friendly to ignore legal implications. Before allowing any agricultural activity on your property, contact your local tax assessor to understand potential consequences.

Essential steps to protect yourself:

- Get written agreements specifying who pays taxes

- Require proof of the user’s agricultural exemptions

- Check with tax authorities before agreeing to any arrangement

- Consider requiring bonds or deposits to cover potential tax liabilities

- Set specific end dates for all arrangements

- Document that activities are temporary and non-commercial when applicable

Tax consultant Jennifer Walsh advises caution: “The agriculture tax system isn’t designed for informal arrangements. Every landowner needs to assume the worst-case scenario and plan accordingly. Friendship doesn’t protect you from tax consequences.”

Margaret’s story serves as a warning about the hidden costs of generosity in our increasingly complex legal landscape. Her agricultural tax bill ultimately forced her to sell a portion of her land – the very outcome she was trying to help Tommy avoid.

FAQs

Can I be held responsible for agricultural taxes even if I don’t farm the land myself?

Yes, property owners are typically responsible for all taxes on their land regardless of who uses it for agricultural purposes.

How long can tax authorities go back when assessing agricultural taxes?

Most states allow 3-7 years of back taxes and penalties once agricultural use is discovered.

Will having beehives on my property automatically trigger agricultural taxation?

If the beehives are part of a commercial operation, yes. Personal hobby beekeeping typically doesn’t trigger agricultural taxation.

Can I require the farmer to pay agricultural taxes in our agreement?

You can create agreements requiring the user to pay taxes, but you remain legally liable if they don’t pay.

What happens if I can’t afford the agricultural tax bill?

Unpaid agricultural taxes can result in liens, penalties, and potentially forced sale of the property.

Are there any exemptions for helping small farmers or beekeepers?

Tax authorities generally don’t recognize “helping” as a reason for exemption. Commercial agricultural use triggers taxation regardless of the landowner’s intentions.